The American Dream has always consisted of grandiose visions of retired life. After working hard for decades, most people want a life of leisure at a later age. But why wait until it’s too late? Why not put in the work now to retire sooner while you’re still young enough to do everything you’ve ever wanted to do in life?

Retiring in your 40s is entirely possible, but it requires a strict budget, smart money moves, giving up unnecessary luxuries, and living a frugal but fun life. Take these 40 steps to get closer to retirement while you’re still young enough to enjoy all of the extra free time.

1. Define What ‘Retired’ Means

The word retirement carries a different meaning for everyone. Some people think of retirement and picture a day filled with nothing but leisure activities, living off investments and savings. Other people picture retirement as a combination of living off saved money while still having a side hustle. Decide what you want your retirement to look like.

2. Write Down a Specific Goal

Saying a goal out loud or telling friends or family about the plan isn’t enough. If you want to reach a goal, you have to write it down. People who describe or picture their goals are more likely to successfully accomplish them than people who don’t.

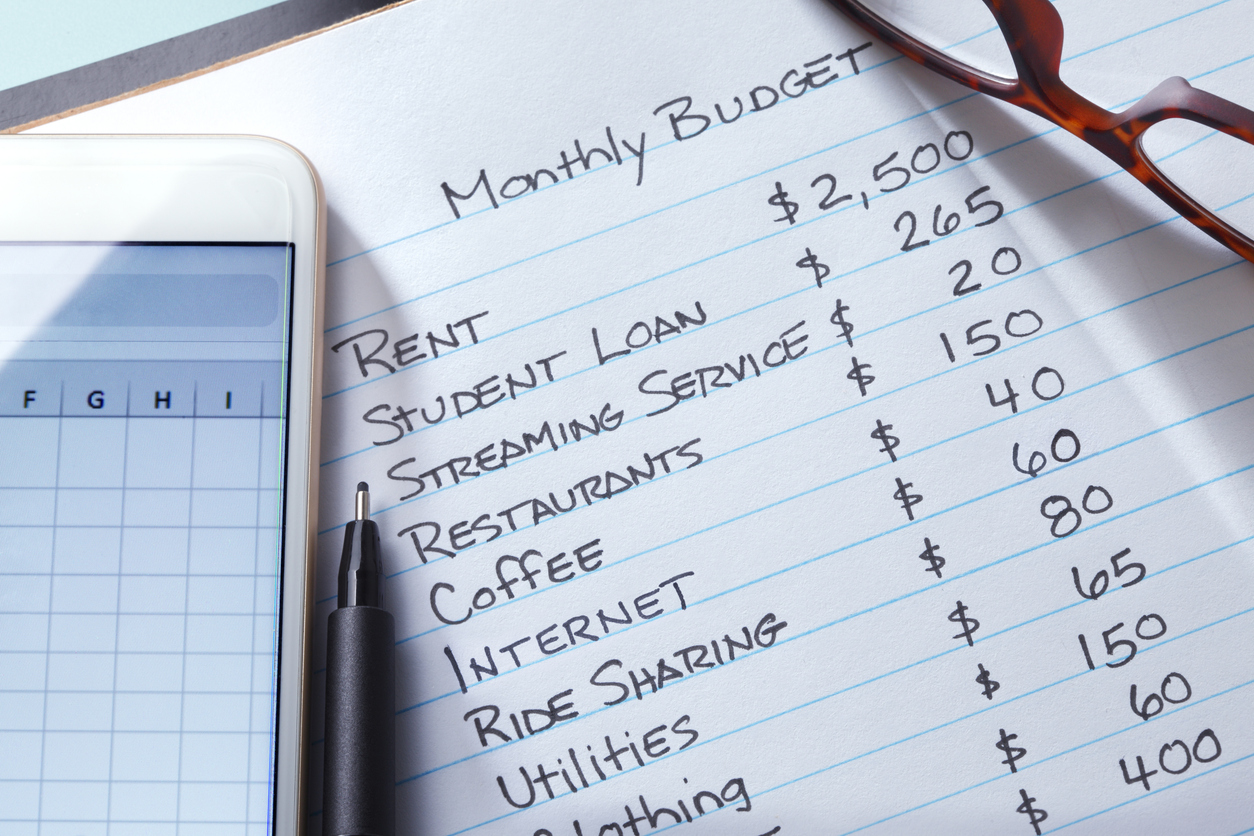

3. Crunch the Numbers

Millions of Americans aspire to retire someday, but it’s impossible to reach that goal if you’re not even sure how much money you’ll need for the rest of your life. To get the exact number, use a retirement income calculator. Once you land on a specific number, write the figure out and thumbtack it somewhere where you’re forced to acknowledge it every single day. Then get a tool to keep track of all your finances.

4. Study People Who Have Done It

If you’re not sure how to fix a leaky faucet, you ask a friend who’s handy with tools or watch a few YouTube videos. If you’re hesitant to sit down on a piece of exercise equipment at the gym, you ask another member using the machine or seek help at the front desk. So why wouldn’t you look for early retirement advice from people who’ve retired early? Cherry pick the best ideas for your own journey to early retire and stick to the plans that work best.

5. Talk to a Financial Planner

After crunching the numbers, you’ll get a better idea if you’re on track to retire in your 40s or if you’re way off base. No matter the result, it’s wise to talk to a financial planner. Everyone, no matter their income level, should speak with a financial planner from time to time. After that, open an investment account. If you’re new to investing, it is probably wise to stick with ETFs (exchange traded funds).

Trending on Wealth Gang

6. Define Your Wants and Needs

The easiest way to find more money to save is to identify the money you’re wasting each month. Go through your credit card bill and bank statement in the last few months. Put a giant “W” (want) or “N” (need) next to each item. Eliminate many of the wants from your spending and instead take that money and deposit the sum right into savings.

7. Tell People You’re Going To Retire Before 50

People set goals and refuse to share these goals out of fear of embarrassment if the goal is never reached. There are many reasons why keeping your goals to yourself is a bad idea. Studies have proven that publicly sharing your aspirations and subsequent progress can actually help motivate you to accomplish your goals. Think of friends, family, and coworkers as accountability partners, each pushing you to reach your retirement goal.

8. Move to a Cheaper City

This suggestion might be tough for people with families, but if you’re single and living in an expensive area, it might be time to pick up and move. Don’t spend all of your extra money on a zip code. Scope out some of the least expensive places to live and do some online research. If the move feels right, start looking for jobs in the area or ask if your current employer would consider letting you telecommute. If moving right now isn’t possible, consider uprooting to one of the top-rated cities for retired people.

Sign up for our newsletter

9. Take Advantage of Employer Matches

About 75% of companies offering 401(k) retirement plans offer some type of matching program. Unfortunately, some surveys show that 1 in 4 Americans fail to take advantage of this free money. This could be a costly mistake for thousands of people and delay retirement plans by decades. Find out if your company matches 401(k) investments and get as much money as possible put away for the future.

10. Think Like Your Grandparents

Previous generations had a simple rule about spending money: If they didn’t have the money, they couldn’t spend the money. It was a straightforward philosophy to follow since credit cards didn’t exist, but one you can still adopt if you want to retire before hitting middle age. If you can’t afford something, don’t buy it.

11. Double Your Savings by Taxing Yourself

The key to saving more money while still making the same salary is to imagine you’re being taxed. Taxes are taken out of each paycheck whether you like it or not, so why not tax yourself? To make sure the “tax” sticks, make it automatic. Set up an automatic payment from your checking to your savings account. The less time the money is in your possession, the less of a chance you’ll talk yourself into mindless spending.

12. Don’t Make Your Money Accessible

Mindlessly using debit and credit cards to pay for items makes it seem as though there’s an endless reservoir of cash available. Give yourself less access to money. If you’re leaving the house, bring only a small amount of emergency cash. Leave the plastic at home. If you’re hesitant to leave the house without a credit card “in case of an emergency,” ask yourself this simple question. “When was the last true emergency that needed your credit card?”

13. Show a Friend Your Spending

People have secrets, and spending habits are sometimes deep, dark secrets. Now imagine that all your spending habits were out in the open for people to view. You’d likely spend less money every month on fancy nut mixes and subscriptions to magazines you never get around to reading. Enlist the help of a trusted friend and give them a peek into your monthly expenditures. Not only will exposure cause you to spend less, but friends can often ask the tough questions you refuse to acknowledge.

14. Adopt a Minimalist Lifestyle

Being a minimalist means living with the very basics. A better way to explain the way of life is adopting the want and need approach to spending money and classifying the items in your life. All of the extra stuff in the garage, spare bedrooms, desk drawers, and kitchen: Do you need those items or did you just want them at some point, never to use them again?

15. Sell Your Life

This concept goes hand-in-hand with the minimalist lifestyle. After decluttering your home, it’s possible to make a killing selling everything online. From eBay to Craigslist and Facebook Marketplace, making a significant sum of money by selling your unwanted goods is the perfect way to jump-start a savings account or knock significant numbers off credit card debt. The items that don’t find a new home can be donated and written off during tax season.

16. Take Advantage of Free Happiness

Buying stuff and spending money doesn’t equal happiness. There are ways to be happy without spending a dime. If you lose focus for a while and put goals aside to help others, it’s always possible to get back on course.

17. Get a Side Job

More than a third of Americans have a side job. This side hustle doesn’t have to take up hours of time or bring in that much money. You can start a blog, sell baked goods at a farmers market, become a dog walker, or tutor — just make sure you’re not sacrificing too much for your free time.

18. Avoid Vacations for Now

Everyone needs a vacation. We’re not advising that you stop taking physical and mental breaks from work. Instead, we’re suggesting eliminating vacations which cost over a month or more of salary. Eliminating this massive expenditure is a no-brainer. Would you rather take a week off and spend it in a tropical locale now or save the money, retire at middle-age, and spend months in that same tropical setting?

19. Delete Your Social Media Accounts

FOMO, or fear of missing out, is a huge reason people spend more money than they make in a year. Instagram stories and Facebook updates make it appear as though everyone is living their best life. If you can’t go on social media without coveting an expensive trip to wine country, a brand new kitchen, or a jacket costing more than a mortgage payment, it might be time to delete your accounts. If this seems too harsh, keep the accounts active and just delete the apps off your phone.

20. Buy a Reliable Car Outright

If you’ve ever listened to financial guru Dave Ramsey (or read any of his books), you’ll know his feelings on the albatross that is the monthly car payment. After mortgage payments, it’s typically the most significant monthly bill for most households. It doesn’t have to be. A car serves only one purpose: to get from point A to point B. All of the other stuff is just a status symbol and showing off. If you want to drive an expensive car, that’s fine. Just make sure the car is completely paid for and not busting your budget month after month.

21. Stop Eating Out

If you want to retire by your mid-40s, you’ve got to limit eating out. People spend substantial amounts of money on restaurants when they could be cooking at home.

22. Create a Retirement Support Group

We all get by with a little help from our friends, so why not hang out with people all working towards the same goal? Being connected to a group of like-minded and goal-oriented individuals is the easiest way to stay on track towards your retirement. Plus, you’ve got a set group of friends to hang out with when everyone else is still going to work every day.

23. Realize a Million Dollars Isn’t Enough

The goal for retirement when our parents were in their earning prime was having a million dollars in the bank. Sadly, retiring on a million dollars just isn’t enough today. If you want to retire in your 40s, you’ll need way more than a million dollars in the bank. You’ll need robust savings, secure investments and even some cash stashed away in case of a significant emergency.

24. Track Your Spending to the Penny

Stop mindless spending. It’s going to curtail your retirement plans. Get an app that tracks your every penny. If you end up with more pennies than you need, reinvest that change with the help of another app. Let technology hold you accountable and keep you pushing toward your goals.

25. Learn To Be More Handy

Time is money. If you don’t have the time, you’re more likely to spend the money, especially on small little projects around the house. Instead of paying a stranger to fix the railing that keeps falling off or to unclog the shower for the tenth time this year, watch a few YouTube tutorials and tackle the issues on the weekend. If you become a master at handling odd jobs, consider making handiwork your own side hustle.

26. Eliminate the Biggest Bills

After creating a budget and listing all your monthly bills, take a long, hard look at the highest numbers at the top of the heap. Besides the mortgage and hefty car lease payment you’re unable to get out of, what are the other massive payments you’re making each month? Find a way to make those payments smaller or eliminate them all together.

27. Get Accustomed to Going Without

Breaking bad habits is hard, especially if your habits include overspending. If you want to retire in your 40s, you’ve got to learn to live well below your means. Especially if retirement means no longer earning a steady paycheck.

28. Never Save Your Credit Card Info

Saving credit card information for express purchasing is the easiest way to overspend. There’s absolutely no work involved. Delete all of your credit card info from shopping websites and on your smartphone. It’s not just helpful for saving money — it also keeps your information safe and secure in case a site gets hacked.

29. Give Yourself 24 Hours on Purchases

Mindless spending is one issue. Impulse buying is an entirely different beast altogether. Instead of dropping money on new running kicks you might not need yet, or walking into a store just because the word “sale” flashes in your face, give yourself 24 hours before buying any item. This is usually enough time to either convince yourself it’s a want and not a need.

30. Stop Buying Brand Names

How many time has this happened: You spend a good sum of money on an expensive sports jacket, dress, purse, or pair of designer shoes, and not one person makes a comment on the item. Then a few days later you’re wearing a $10 shirt, and people can’t stop asking, “Where did you get that?!?” No one really cares about brand names. It’s all about style and the way you present yourself. Start presenting your best self in less expensive clothing.

31. Switch to Cash Only

There’s a reason people overspend or go into credit card debt. It’s so easy just to swipe a card and get whatever your heart desires. If you can’t trust yourself with plastic, leave all the cards at home. If that doesn’t work, hit the bank after payday, take out all the cash, and stuff it in a drawer. Cut up the credit cards. Stick them in a cup of water and leave them in the freezer. Make it impossible to use debit and credit cards.

32. Turn Cash Into Change

If the cash in your drawer is calling your name, turn it all into change. There’s a good chance you’ll cheat and grab a $20 to get pizza or buy a handful of lottery tickets for fun. There’s very little chance you’ll walk around with 80 quarters in your pocket.

33. Don’t Buy Lunch, Coffee, or Bottled Water

The average cup of regular coffee costs about $1.50. Expensive coffee drinks at Starbucks or high-end coffee shops can cost as much as $8. The average bottle of water at lunch is about $1.50. Those numbers add up over weeks, months, and years. Get a water filtering system and carry around a refillable bottle of water. Brew your own coffee at home. If a coworker or friend asks to meet up for coffee, tell them just to give you a call and save the money. Take the combined money saved and put it into a savings account on top of the money you’re already saving.

34. Lose Some Friends

Maybe cutting ties with friends is a little extreme, but friends present the constant pressure of getting together for dinner, drinks, group trips, and hundreds of other ways to spend large sums of money. Either trim your inner circle to only your closest friends or just go out for special occasions like birthdays or around the holidays. The easiest way not to keep up the Joneses is to stop hanging out with them all together.

35. Get on the Same Page With Your Partner

Retiring by the age of 40 isn’t going to happen unless you and your significant other are on the same page with both saving and spending. What good is saving money and keeping a budget if your spouse is blowing it all on extra expenses and not saving a dime for retirement? A great way to track this is to use a tool to get total control over your joint finances.

36. Shop Secondhand

New looks nice, but sometimes buying items brand new is pointless and pricey. There are hundreds of items that should never be bought new, including books, tools, cars, sports equipment, baby items like strollers and clothing, and even some furniture.

37. Review Your Goals Weekly

The easiest way to lose track of your goals — or never reach them at all — is to stop tracking your progress. Even if you’re completing all the necessary steps, it’s vital to track progress and tweak your goals each month. Are you saving all the money you can save? Are you wasting money in certain areas? Have some investments started paying more than others? Is there a way to make even more money on a side hustle?

38. Celebrate Small Victories

Even though you’re planning for retirement, the day you quit the working world is likely a long way off. While it’s the eventual goal, you’ve got to celebrate small victories along the way. Tracking small victories is a motivational technique. The little wins keep you going. Celebrate those wins without spending, and you’ll likely find yourself rejuvenated and ready to take on the next hurdle towards a leisured life.

39. Book a Retirement Party

Pick the year, pick the exact date, find a venue, and put down a deposit for your retirement party. If you don’t want to spend the money now, send an Evite for a party at your house on a specific day. Now that you’ve got a plan and a day in mind, get to work so you’ll never have to work again!

40. Trust the Process

It will be tempting to make many of these moves in a short period of time. While drastic change is often necessary for real amendments to the way a person lives life, it’s important to climb one mountain at a time.

Want more retirement advice?

If you’re in the throes of planning for retirement — whether it’s an early one or not — be sure to read 9 Money Mistakes That Could Wreck Your Retirement Plan and 5 Warning Signs That You’ll Run Out of Money in Retirement. You may also want to check out How Long Will My Money Last? The Question All Retirement Seekers Must Ask.