A couple of years ago, I had to take a long, hard look in the mirror about my savings habits. I wasn’t hurting. But I also wasn’t thriving. This was driving me crazy. I wanted to thrive.

Some context: A cross-country career move from New York City to Los Angeles was starting to evaporate my savings. I moved to Los Angeles in 2017, excited to grow my career prospects.

At the time, I had a great job working with great people for (what seemed like) a great company.

I aspired to grow my career in that company with skills and a creative playbook valuable to other, bigger companies in the same industry.

I was excited about a new chapter.

As a perpetual networker, my job at the nexus of digital content and advertising was a fast-paced and thrilling one: I planned and executed collaborative ideas for major advertising partners, creating crucial advertising revenue for a website I had helped build years earlier.

Los Angeles, to me, seemed like the center of that industry. The company I worked for was one of a handful of players figuring out how to do branded content the right way on mediums like Facebook, YouTube, and Snapchat.

I was involved in almost every aspect of the advertising process: Brand strategy, proposals, proactive pitches, production, distribution, and reporting. Then we’d build case studies to show what we’ve done and do it all over again.

I can say I built and helped produce some major campaigns I’m incredibly proud of: Netflix, Dockers, Jägermeister, Viacom, Activision, Warner Brothers, Electronic Arts.

Things felt like they were going great, that I was hitting my career stride.

I felt like I was about to climb into the cockpit of a career rocketship right before blastoff.

Except that rocketship failed to ignite on the launchpad.

A couple of months after arrival, the company I was working for announced they were in the process of selling and downsizing. I’d have to start over from scratch in a new city that I didn’t really know. I had many acquaintances in Los Angeles but few career contacts and even fewer close friends.

I had already sunk some of my savings into the things one spends money on when California comes a-callin’. A modest apartment that I loved, in a quiet neighborhood that I loved as well. Furnishing said apartment. Buying a car. Building out a social calendar with my significant other to explore our new city, along with building new friendships.

Meanwhile, my family? They were on the other side of the country, cautiously questioning what I’d do next.

In short order, a new career opportunity presented itself.

It was somewhat of a lateral move. It also involved betting on myself and the business value I could provide. The digital business had a strong audience, assets, and name recognition, but the actual business opportunity was far from stable. It involved architecting and acting upon a vision from square one.

I had to go back to head down, grind mode.

The people I talked to and worked with every day at the old job? All gone, except for an occasional lunch or drinks to catch up.

I’m no stranger to career leaps of faith. I’ve worked in entrepreneurial, start-up environments for practically my entire career. The day-to-day isolation and building ethos that it takes didn’t bother me.

Being on a career rollercoaster didn’t even really bother me.

But where I was at financially sure did.

As someone rapidly barreling towards their mid-30s and my peak earning years, I couldn’t help but feel that I was off track.

Here I was, 33 years old in a city with an awfully high cost of living, with very few assets to my name, let alone a financial plan for retirement and settling down to start a family.

I especially felt this way with my savings.

I automatically deducted a certain amount of each paycheck to my savings account, but once it was there, it just sat there.

Disclaimer: This is not financial advice. I am not a financial adviser. Just a very happy Acorns customer sharing my experience with the Acorns aggressive portfolio.

Then I saw an ad for Acorns on Reddit.

I was haplessly browsing r/personalfinance one day, and there it was: An ad for a savings and investment tool called Acorns on Reddit.

Ever wonder who actually looks at ads on websites? Some people say you have to be a crazy person to browse the Internet without AdBlock these days.

Well, that’s me.

I’m the dork who actually looks at the ads on websites, mostly because it’s how I’ve been able to make a living over the years.

I thought the ad was a really creative one.

The premise for Acorns piqued my curiosity.

I dug in deeper.

As I recall, the ad mentioned how Acorns could help you save and invest spare change from credit card transactions, then depositing it into a brokerage account where it had the potential to earn more interest than parking it in a savings account.

I’m the sucker where Acorns’ paid advertising actually worked.

Trending on Wealth Gang

I liked the idea of starting small with new savings habits.

Acorns reminded me of how I’d save money as a kid before my first real job (at age 15, in a music store in my hometown!), putting money from odd jobs and chores in a coffee can. Mow the neighbor’s lawn or shovel snow, put $10 earned aside, and don’t even think about it until that can is full.

These habits are how I saved for some of my prized possessions as a kid: A stereo for my bedroom, a 21-speed Murray mountain bike, Nintendo 64 games, etc.

Why shouldn’t the same principle apply to saving in adulthood?

When I signed up for Acorns, I started with the Acorns conservative portfolio. I wanted to think about it as a secondary savings account.

I wasn’t really ready to take a big risk with Acorns yet – most of my focus in building bigger savings habits was also on ways to generate more income, including with really simple side gigs and hustles.

After being solely focused on my career for years, I wanted to change my way of thinking about money beyond just the confines of that job.

Chalk this attitude up to trauma from having my job security wiped out after a major life move, then having those expectations go sideway.

For example, as a California resident, I saved big piles of aluminum cans in my kitchen, then deposited them at the grocery store. No one really gets rich doing this, of course, nor did I really have the space for it. And the smell… oh boy, the smell. But this became a healthy habit for me, teaching me what “found money” really meant.

The $5 or $10 I made, I’d deposit the same amount into Acorns.

I also charged electric Bird and Lyft scooters that popped up around my neighborhood, earning some spare dollars upon returning them to their spots in the morning.

It’s a hard side hustle to commit yourself to truly, but it became a fun hobby for learning more about my neighborhood and city.

When I received birthday money from my Mom or grandparents to “take myself out for a good meal,” I’d deposit an equal amount into Acorns as a matter of habit to see that money start accruing interest in the market.

I’d still honor their wishes and take myself out – life is just too short, after all – but I’d recalibrate my day-to-day spending on that specific splurge.

Maybe it meant staying home to watch an NFL game on Sunday instead of meeting up with friends at the bar. Or doing a week of peanut butter and jelly sandwiches for lunch instead of a $10 salad. Or shopping for new business-appropriate clothes at Costo, where they were much cheaper, instead of from a DTC menswear company online.

I was starting to see the vision for how this could work—$ 5 here, $7 there.

It all adds up over time.

After a couple of months and saving money that I probably otherwise wouldn’t have, my attempt to growth-hack my personal financial habits was working.

I was recalibrating my habits and saving in a way I hadn’t before.

Sign up for our newsletter

And I was just getting started with Acorns.

After seeing my initial savings from Acorns and its application to my overall financial portrait, I started thinking about Acorns like an engine.

An engine has an everyday purpose and function in a vehicle: To get you where you want to go, safely and enjoyable. But it requires disciplined upkeep (IE: an oil change every 3,000 miles) and constant attention – even if subconsciously – to run at maximum efficiency.

Hear something that sounds off? Better get it checked out.

The more you see that engine work for you, the better you’ll start to take care of it.

In Acorns’ case, the fees associated with keeping the engine running – $1 a month up to $1M in account value – seemed reasonable.

After a couple of months, I set up weekly reoccurring deposits in Acorns, in addition to round-ups with a multiplier (3x).

This was the beginning of my set-it-and-forget-it approach. I then changed it to a daily deposit, of which I’ve continued to grow up over the past two years, depending on my income levels.

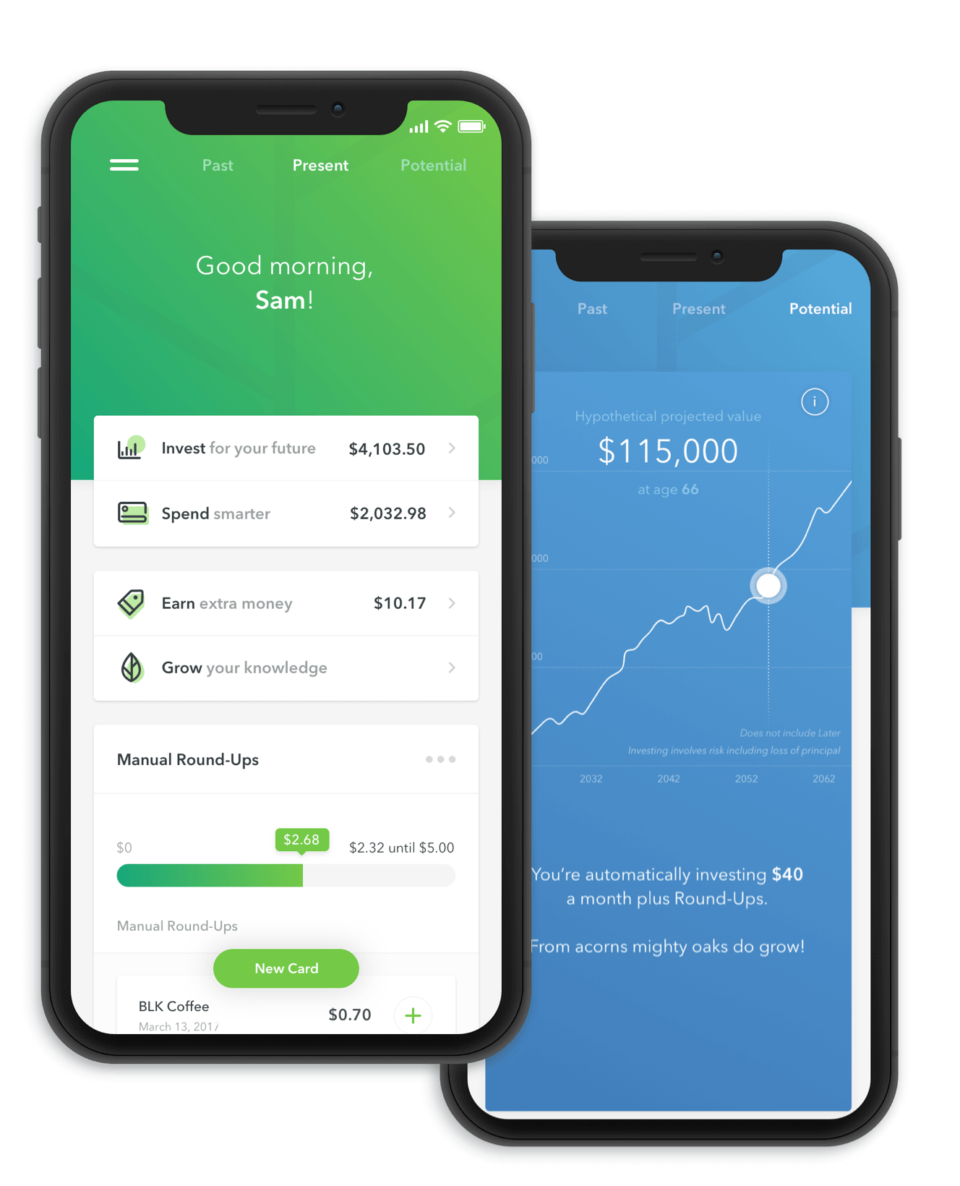

![]()

Acorns Aggressive Portfolio – My Personal Savings Engine

After a little research and lurking in the r/Acorns Reddit community, in 2019, I moved from a conservative portfolio to the Acorns aggressive portfolio to start maximizing my investment potential. My thinking: I’m not really a fan of picking individual stocks or ETFs (I constantly lose with that strategy), yet the US stock market is currently on its longest bull-run in history.

Gotta be in it to win it.

I started thinking about how Acorns can, hopefully, help me reach my long-term financial goals, like buying a house, starting a family, and retirement.

As a day-to-day user, I enjoyed watching the automatic DRIP money going into my Acorns aggressive portfolio. It also meant dividends from ETFs like VOO accrue while further tightening my spending habits.

I also started discovering ways to use Acorns’ found money marketplace when I needed it. For example, earlier this year, I needed a new laptop for work after the battery in my old one started to wear out. I earned $60 from Apple from the purchase, deposited it into my Acorns account as an investment when I bought it via the Found Money marketplace.

It all goes to the goal.

I haven’t used services like Acorns Later – the Acorns retirement tool for IRAs – or Early, for family financial planning.

I do plan on it using these Acorns services in the future, though, based on my current experience with the Acorns aggressive portfolio. Of course, things can change – It’s the only constant in life.

There are five Acorns portfolios when you go to set up your account. As an Acorns customer, these can be changed over the course of your investing journey, depending on your financial situation.

The Acorns profiles themselves are comprised of popular ETFs:

- Conservative – This is the least risky Acorn portfolio. It’s comprised of short term government bonds (40%), ultra short term corporate bonds (40%), ultra short term government bonds (20%)

- Moderately Conservative – This is mostly made of large-company stocks (24%) and government and corporate bonds (60%), along with medium company stocks (4%) and international company stocks (12%)

- Moderate – Comprised of large-company stocks (35%), medium company stocks (5%), small company stocks (2%), international company stocks (18%), government & corporate bonds (40%)

- Moderately Aggressive – Comprised of large-company stocks (47%), medium company stocks (6%), small company stocks (3%), international company stocks (24%), government and corporate bonds (20%)

- Aggressive- Comprised of large-company stocks (55%), medium company stocks (10%), small company stocks (5%), and international company stocks (30%). If time is on your side, the Acorns aggressive portfolio might be for you.

In conclusion

I’m not going to tell you how much I’ve put aside in my Acorns portfolio. Just know that I’m thrilled with it at the moment. If you want to see specific examples of market gains, there are many all over the r/Acorns sub-Reddit.

And, of course, please note that none of this is financial advice. This is just my first-hand experience using the app.

The difference I’ve seen in three years of using Acorns is astounding – largely due to (A. modifying my savings habits and (B. compounding interest from my portfolio.

You really do start to see why Acorns built its entire brand around a 14th century English proverb:

“Mighty oaks grow from little acorns.”

I met with a financial adviser years ago who asked me about my savings goals for certain ages. At the time, I had no plan. Zero. I just knew I wanted a house and the luxury of (hopefully) not working someday.

I was the proverbial clueless millennial, wandering through the desert about how to truly save money. Instead of recommending a practical tool for savings, he tried to sell my life insurance in that meeting.

The sales pitch bothered me; I ghosted him after that.

I didn’t forget the discussion, however. Instead, I just looked for new tools to pivot my philosophy and figure it out myself.

When that presented itself, I ran with it.

Acorns – and a little personal agency in my own finances – put me well on the path to a big goal we discussed in the meeting.

For that, maybe I owe the guy a thank you?

For years, I was worried that I was starting too late. That lead to some analysis paralysis on what to actually do and how.

Acorns and, specifically the Acorns aggressive portfolio somewhat help fill that void.

Even better, reassured me that I wasn’t really as far off the path as I thought I was.