When it comes to managing money, we’ve all fallen prey to money myths that sound logical but actually end up biting us in the wallet. From the idea that skipping coffee will make you rich to the belief that carrying a credit card balance can boost credit scores, these money lies can often lead to poor financial habits.

The truth is that many of these misconceptions are rooted in oversimplified advice or outdated thinking. To help you separate fact from fiction, here are 10 common money lies you might still believe in.

1. ‘I’ll Save What’s Left at the End of the Month’

This approach rarely works because, let’s be honest, there’s usually nothing left at the end of the month after all the bills are paid. Instead, prioritize saving by setting up automatic transfers to your savings account as soon as you get paid (you can start small and gradually increase over time). By treating savings like a non-negotiable bill, you’ll be able to build a financial cushion effortlessly without even thinking about it.

2. ‘Renting Is Throwing Money Away’

Sure, while it’d be ideal to make payments towards a house you’ll eventually own, renting isn’t throwing money away — it’s paying for a place to live. Plus, buying a home isn’t all rainbows and butterflies, and it comes with its own set of hefty costs, such as maintenance, property taxes, closing fees, and interest on a mortgage. In fact, renting can be a smarter choice if you value flexibility, get tired of living in the same place after a while, or live in an expensive or unstable housing market.

3. ‘It’s Easy To Make Passive Income’

Passive income doesn’t mean that the money is going to flow right in. In reality, a lot of upfront work goes into generating passive income streams, and it can take months or years before you start making money from your side projects. Even after you set everything up, you’ll need to monitor your income streams and make sure they’re receiving necessary maintenance.

4. ‘Skipping That Cup of Joe Will Make Me Rich’

While cutting small expenses can help, skipping your daily latte won’t magically solve your money woes. (Though we agree these $7 lattes are getting out of hand.) The real key is focusing on bigger expenses like housing, transportation, and dining out and making sure you aren’t spending more than what you can comfortably afford. That said, if your daily coffee habit adds up to hundreds of dollars a month, it might be worth exploring more affordable options like making your daily brew at home.

5. ‘I Can Always Rely on Social Security’

While Social Security can provide some income in retirement, it’s not enough to live on comfortably. In fact, most seniors rely on it to cover only a portion of their expenses. Benefits may also be reduced in the future due to funding challenges, especially as the newly-appointed Department of Government Efficiency (DOGE) makes massive cuts to federal agencies.

Trending on Wealth Gang

6. ‘Buying in Bulk Always Saves Money’

Buying in bulk can be a great deal — but only if you actually use everything you buy. Otherwise, you’re just wasting money on items that end up expiring or collecting dust in the pantry. Before stocking up, ask yourself if you’ll truly use the quantity and if the upfront cost fits your monthly budget. If not, consider splitting bulk purchases with a friend to save money while reducing waste, or only buying non-perishable items in bulk.

7. ‘Carrying a Balance on a Credit Card Helps Your Credit Score’

This is a dangerous myth. Carrying a balance does not help your credit score; it just ends up costing you interest (and credit card companies typically tack on a hefty fee for late or missed payments). What actually matters is paying your bill on time and keeping your credit utilization low. It’s always best to pay off your balance in full each month to avoid these fees and keep your credit health in top shape. You can also set up reminders or automatic payments to help with this.

8. ‘I Don’t Make Enough To Start Investing’

You don’t need to be wealthy to start investing. Thanks to apps and financial platforms that allow you to invest small amounts, even $10 a month can grow over time. Remember: The earlier you start, the more you’ll benefit from compound interest.

Sign up for our newsletter

9. ‘I Need a High Income To Be Financially Secure’

Financial security isn’t just about how much you earn — it’s also about how much you save and spend. Plenty of high earners live paycheck to paycheck, while others with modest incomes build wealth through smart budgeting and investing.

10. ‘I’m Too Young To Worry About Retirement’

The earlier you start saving for retirement, the better. Thanks to compound interest and retirement benefits, even small contributions in your 20s can grow over time. Waiting until you’re older means you’ll have to save much more to catch up. To bolster your retirement fund, take advantage of employer-sponsored plans like a 401(k), especially if they offer matching contributions. If that’s not an option, open an IRA account and contribute consistently, even if it’s just a small amount.

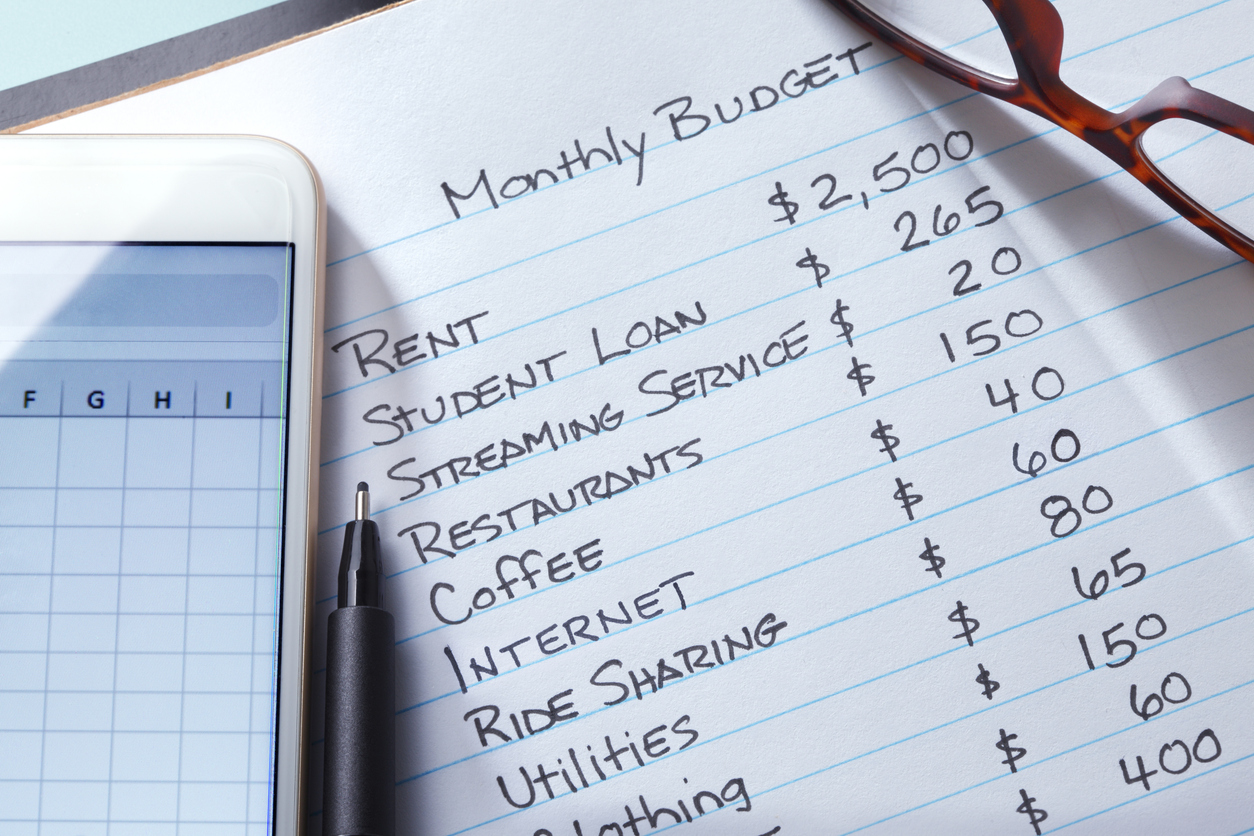

11. ‘I’ll Start Budgeting When I Make More Money’

Budgeting isn’t just for people with tight finances — it benefits everyone (unless you’re a billionaire, of course). No matter how much you earn, a budget can help you track spending, practice discipline, and avoid debt. The sooner you start, the more control you’ll have over your money, and the closer you’ll be to reaching your financial goals. Consider using tools like budgeting apps or spreadsheets to make the process easier and more seamless.

Need more money advice?

- 11 Psychological Tricks That Drain Your Wallet — Discover almost a dozen money mind tricks, plus tips on how to identify them before they put a hole in your wallet.

- 10 Money-Saving Tricks Our Grandparents Swore By (That Still Work!) — Here are 10 clever hacks our grandparents swore by that still ring true today.

- 8 Ways Going Green Actually Saves You Money — From simple home hacks to making smarter daily choices, going green delivers savings that compound over time.